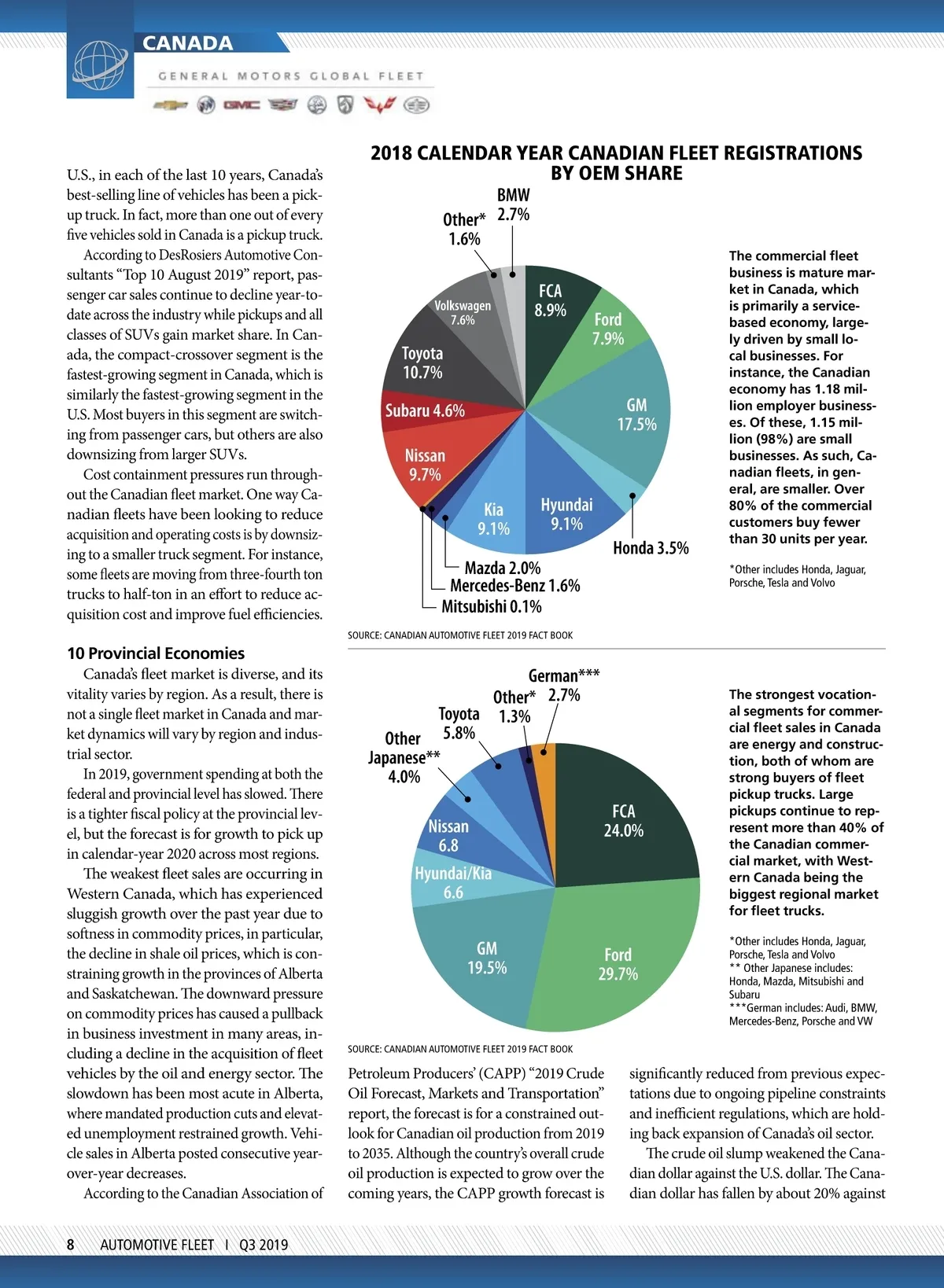

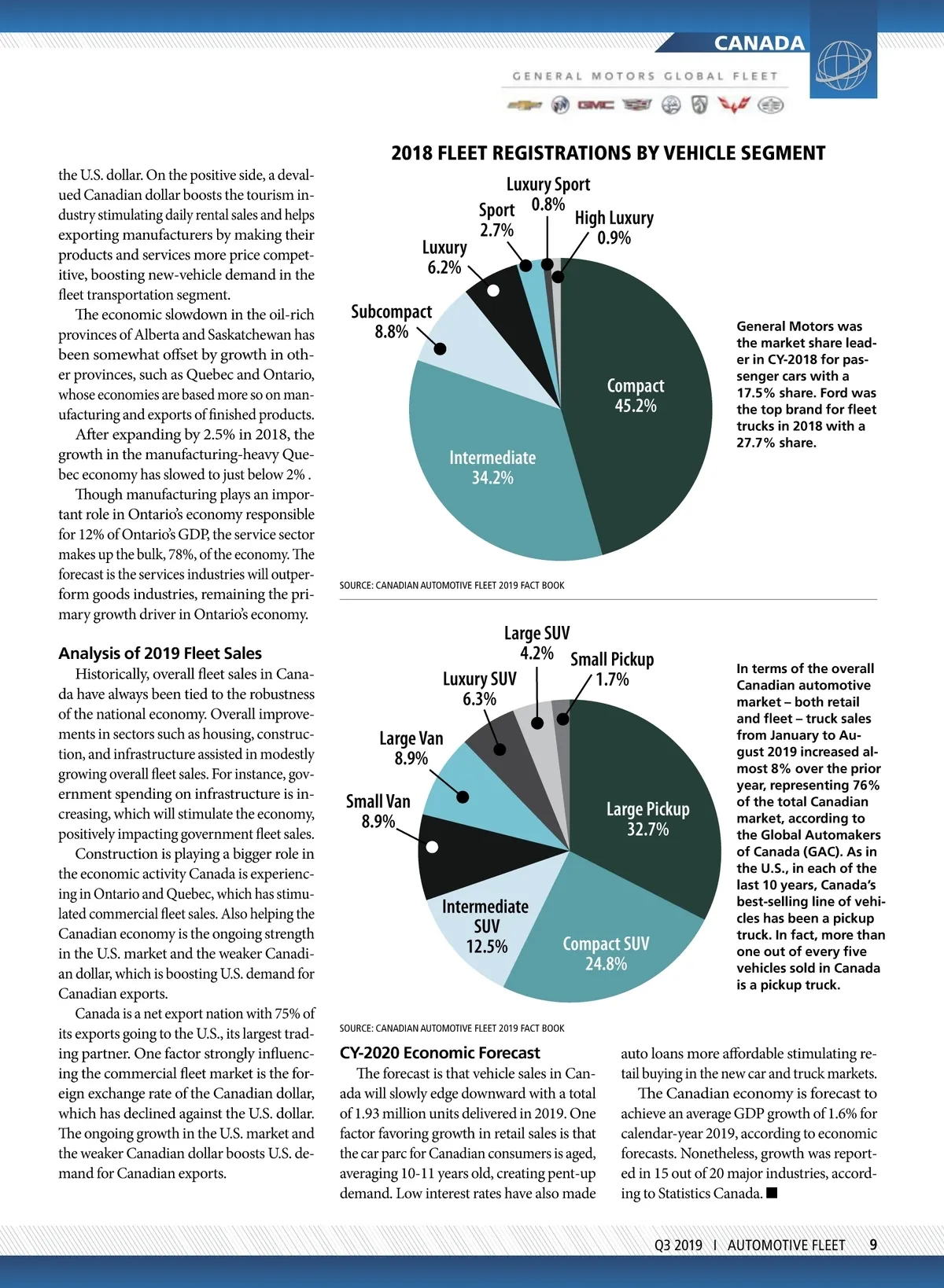

CANADA 2018 FLEET REGISTRATIONS BY VEHICLE SEGMENT the U.S. dollar. On the positive side, a deval-ued Canadian dollar boosts the tourism in-dustry stimulating daily rental sales and helps exporting manufacturers by making their products and services more price compet-itive, boosting new-vehicle demand in the leet transportation segment. he economic slowdown in the oil-rich provinces of Alberta and Saskatchewan has been somewhat ofset by growth in oth-er provinces, such as Quebec and Ontario, whose economies are based more so on man-ufacturing and exports of inished products. Ater expanding by 2.5% in 2018, the growth in the manufacturing-heavy Que-bec economy has slowed to just below 2% . hough manufacturing plays an impor-tant role in Ontario’s economy responsible for 12% of Ontario’s GDP, the service sector makes up the bulk, 78%, of the economy. he forecast is the services industries will outper-form goods industries, remaining the pri-mary growth driver in Ontario’s economy. Luxury Sport Sport 0.8% High Luxury 2.7% 0.9% Luxury 6.2% Subcompact 8.8% Compact 45.2% Intermediate 34.2% General Motors was the market share lead-er in CY-2018 for pas-senger cars with a 17.5% share. Ford was the top brand for leet trucks in 2018 with a 27.7% share. SOURCE: CANADIAN AUTOMOTIVE FLEET 2019 FACT BOOK Analysis of 2019 Fleet Sales Historically, overall leet sales in Cana-da have always been tied to the robustness of the national economy. Overall improve-ments in sectors such as housing, construc-tion, and infrastructure assisted in modestly growing overall leet sales. For instance, gov-ernment spending on infrastructure is in-creasing, which will stimulate the economy, positively impacting government leet sales. Construction is playing a bigger role in the economic activity Canada is experienc-ing in Ontario and Quebec, which has stimu-lated commercial leet sales. Also helping the Canadian economy is the ongoing strength in the U.S. market and the weaker Canadi-an dollar, which is boosting U.S. demand for Canadian exports. Canada is a net export nation with 75% of its exports going to the U.S., its largest trad-ing partner. One factor strongly inluenc-ing the commercial leet market is the for-eign exchange rate of the Canadian dollar, which has declined against the U.S. dollar. he ongoing growth in the U.S. market and the weaker Canadian dollar boosts U.S. de-mand for Canadian exports. Large SUV 4.2% Small Pickup Luxury SUV 1.7% 6.3% Large Van 8.9% Small Van 8.9% Large Pickup 32.7% Intermediate SUV 12.5% Compact SUV 24.8% In terms of the overall Canadian automotive market – both retail and leet – truck sales from January to Au-gust 2019 increased al-most 8% over the prior year, representing 76% of the total Canadian market, according to the Global Automakers of Canada (GAC). As in the U.S., in each of the last 10 years, Canada’s best-selling line of vehi-cles has been a pickup truck. In fact, more than one out of every ive vehicles sold in Canada is a pickup truck. SOURCE: CANADIAN AUTOMOTIVE FLEET 2019 FACT BOOK CY-2020 Economic Forecast he forecast is that vehicle sales in Can-ada will slowly edge downward with a total of 1.93 million units delivered in 2019. One factor favoring growth in retail sales is that the car parc for Canadian consumers is aged, averaging 10-11 years old, creating pent-up demand. Low interest rates have also made auto loans more afordable stimulating re-tail buying in the new car and truck markets. he Canadian economy is forecast to achieve an average GDP growth of 1.6% for calendar-year 2019, according to economic forecasts. Nonetheless, growth was report-ed in 15 out of 20 major industries, accord-ing to Statistics Canada. ■ Q3 2019 I AUTOMOTIVE FLEET 9

Automotive Fleet Nov 2019: 9